China's Housing Bubble?

Earlier this week, a quick, two sentences from The Economist jumped out at me as the most important part of a long article on the Chinese economy. China “struck a hawkish note on the eve of the [Politburo] conference, promising to remain ‘unswerving’ in its campaign against property-market speculation. That sent Shanghai’s stock market index down to its lowest level since March 2009, with property developers suffering especially.” Next to this magazine column, I scribbled a note to myself to ask a friend in real estate whose firm is looking to develop land in China about what sounded like the popping of a bubble. This could spell trouble for new city development in the region, especially since Chinese officials are starting to worry about clear signs of excessive speculation.

|

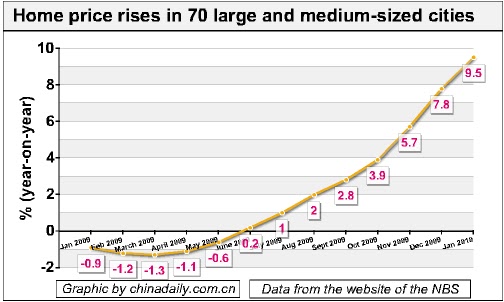

| Rising home prices in China cause need to worry. |

Yesterday, Paul Krugman, voiced similar worries about the Chinese real estate bubble. “Real estate investment has roughly doubled as a share of G.D.P. since 2000, accounting directly for more than half of the overall rise in [China’s] investment…which has soared to almost half of G.D.P.” He continued, “As credit boomed, much of it came not from banks but from an unsupervised, unprotected shadow banking system…In China as in America a few years ago, the financial system may be much more vulnerable than data on conventional banking reveal.”

It is wrong to conclude that China does not need more housing – it clearly needs to provide modern living amenities for its urbanizing population – but bubbles are less about housing demand than about credit crunches. Often times, overly cheap access to credit and rapidly rising real estate prices lead to imbalances in housing supply and demand. Instead of treating housing as a home for living, it becomes a tradable commodity. In the US, for example, the recent housing crash did not occur in reaction to a sudden drop in demand for homes for people to live; the population keeps growing. However, among other causes, inconsistencies in financial markets led to housing prices (as a commodity) dropping below the value of mortgages, leading to people accepting foreclosure when real estate market prices fell below existing mortgage balances.

As both The Economist and Dr. Krugman noted, reliable data from the Chinese are closely guarded secrets, the truth about real estate markets remains murky. Investors, instead of relying on market indicators, should pay attention to the government’s attack on speculation and its signaling pre-emptive acknowledgement of boom-bust market cycles (which in China may already be too far underway to steer against the current). Over-exuberance should always be reason to question the status-quo. Chinese government action should be as well.

0 comments:

Post a Comment