"The United States will add a new inhabitant every 17 seconds and an immigrant every 46 seconds." -- El Deber on the US Census

Thursday, December 29, 2011

Tuesday, December 20, 2011

China's Housing Bubble?

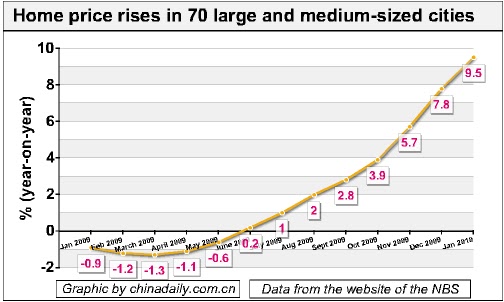

Earlier this week, a quick, two sentences from The Economist jumped out at me as the most important part of a long article on the Chinese economy. China “struck a hawkish note on the eve of the [Politburo] conference, promising to remain ‘unswerving’ in its campaign against property-market speculation. That sent Shanghai’s stock market index down to its lowest level since March 2009, with property developers suffering especially.” Next to this magazine column, I scribbled a note to myself to ask a friend in real estate whose firm is looking to develop land in China about what sounded like the popping of a bubble. This could spell trouble for new city development in the region, especially since Chinese officials are starting to worry about clear signs of excessive speculation.

|

| Rising home prices in China cause need to worry. |

Yesterday, Paul Krugman, voiced similar worries about the Chinese real estate bubble. “Real estate investment has roughly doubled as a share of G.D.P. since 2000, accounting directly for more than half of the overall rise in [China’s] investment…which has soared to almost half of G.D.P.” He continued, “As credit boomed, much of it came not from banks but from an unsupervised, unprotected shadow banking system…In China as in America a few years ago, the financial system may be much more vulnerable than data on conventional banking reveal.”

It is wrong to conclude that China does not need more housing – it clearly needs to provide modern living amenities for its urbanizing population – but bubbles are less about housing demand than about credit crunches. Often times, overly cheap access to credit and rapidly rising real estate prices lead to imbalances in housing supply and demand. Instead of treating housing as a home for living, it becomes a tradable commodity. In the US, for example, the recent housing crash did not occur in reaction to a sudden drop in demand for homes for people to live; the population keeps growing. However, among other causes, inconsistencies in financial markets led to housing prices (as a commodity) dropping below the value of mortgages, leading to people accepting foreclosure when real estate market prices fell below existing mortgage balances.

As both The Economist and Dr. Krugman noted, reliable data from the Chinese are closely guarded secrets, the truth about real estate markets remains murky. Investors, instead of relying on market indicators, should pay attention to the government’s attack on speculation and its signaling pre-emptive acknowledgement of boom-bust market cycles (which in China may already be too far underway to steer against the current). Over-exuberance should always be reason to question the status-quo. Chinese government action should be as well.

Sunday, December 11, 2011

The Atlas of Economic Complexity

|

| As complex as it looks. (Click the graphic to enlarge or here for a key that explains each sector.) |

The recently published the Atlas of Economic Complexity provides a new way to assess and predict future economic growth. Existing measures, like GDP and PPP, ignore the true intricacies of entire economies and fail to capture essential externalities. The Index of Economic Complexity on the other hand accounts for a wider understanding of the capitalist system by acknowledging that markets are aggregates of networks of millions of highly specialized individuals.

Although I personally have yet to explore the specific formulas used to calculate the Index of Economic Complexity (they're as complex as the name suggests), the idea behind the new measure sounds extremely intriguing. On first glance, the Atlas of Economic Complexity appears to be a Moneyball revolution, using advanced statistical data to extract value in areas where status quo measures are long overdue for an modernizing overhaul.

Some quotes:

"The wealth of nations is driven by productive knowledge," writes Ricardo Hausmann, one of the Atlas of Economic Complexity report's primary authors. "Individuals are limited in the things they can effectively know and use in production so the only way a society can hold more knowledge is by distributing different chunks of knowledge to different people. To use the knowledge, these chunks need to be re-aggregated by connecting people through organizations and markets...In fact, [the Index of Economic Complexity] beats measures of competitiveness such as the World Economic Forum's Global Competitiveness Index by a factor of 10 in predicting growth for the following decade. It also beats by similar margins measures of human capital and governance."

The Economist describes the Atlas's ability to explain previously inexplicable trends. "Investment in education is a weaker predictor of economic growth than the complexity measure. The comparison of Ghana, which had invested heavily in education, and Thailand which hasn't, is interesting. Thailand does well in the complexity index and Ghana doesn't. Thailand 'has moved from producing jute and sugar to becoming a major manufacturing center.' Ghana hasn't....The research makes clear that a country can only shift into new more technical products and services along a ladder of existing products through the evolution its productive knowledge in a virtuous circle."

Wednesday, December 07, 2011

Cities on the Sea

|

| Source: Seasteading.org |

“Taxation without representation” still rings true for many libertarians. The possibility to break off from a mother country to create an autonomous self-governing city-state is a possibility that is gaining traction and funds from wealthy backers. Since governments lay claim to all land across the globe, wealthy libertarians, like Peter Thiel, the founder of PayPal, and Patri Friedman, the grandson of Milton Friedman, assembled a think-tank, the Seasteading Institute, to study the feasibility of creating a floating, off-shore city that remains out of reach of national governments. “Our Mission,” writes the Institute on their website, “to further the establishment and growth of permanent, autonomous ocean communities, enabling innovation with new political and social systems."

|

| Source: Seasteading.org |

The Seasteading Institute explores cruise-ship style offices, apartments, and retail centers, which unfortunately cannot withstand the storms of the high seas. Oilrigs provide other platforms, but can cause seasickness when they rock with waves. And cities built above small island foundations raise problems with international law, as these would fall within the grey area of countries’ territorial waters (12 miles offshore) and their exclusive economic zones (200 miles offshore).

|

| A futuristic shipyard in outer space Source: OnRPG.com |

While libertarians are quickly written off as fanatics who wish for the yesteryears of 1776 colonial rebellion, those who dream of cities in space are accepted by society as sci-fi futurists – yet the two concepts are extremely similar. A leading presidential candidate has even suggested the building of "a massive new program to build a permanent lunar colony to exploit the Moon's resources." Ocean city designs would most likely draw ideas of self-sustaining agriculture and energy uses from prior outer space living competitions. Likewise, future space cities would adopt successes and note failures of condensed sea living. While the libertarian city on the sea dream attempts to break barriers to free market concepts (like the uninterrupted movement of labor that could be lubricated with the elimination of visa or immigration laws), those idealists ignore the more cost effective existing terrestrial zones that already cater to libertarian freedoms.

|

| Source: The Economist |

Pushing political views aside and looking at cities on the sea from the Seasteading Institute’s point of view as a creative exercise, these think tanks get funding to conceptualize what it would take to build a new country from scratch in the modern era. They also get to explore designs of how to feed and sustain populations disconnected from traditional terrestrial living. While floating metropolises may be only slightly more realistic at this point than building a real life Death Star in space, ocean-based cities rethink traditional models of urban living. At the very least, the Seasteading Institute’s studies will demonstrate ways to integrate sustainability techniques with underlying urban infrastructure.

For more on Seasteading and floating communities, read The Economist's Seasteading: Cities on the Ocean.

Thursday, December 01, 2011

"Most of the [new city Songdo] will be wired with digital synapses—from the trunk lines running beneath the streets to the filaments branching through the walls and fixtures. To what end? [Songdo's developer] Stan Gale and his partners at Cisco Systems aren’t sure, but imagine if a city operated like an iPhone—and they could sell apps for everyday life..." — Greg Lindsay, City-in-a-Box 11/26/2011

Subscribe to:

Comments (Atom)

{kind=link}